How can I turn my credit into cash without a cash advance? If you’re searching for other ways to get cash without relying on a credit card cash advance, here are some options from York Credit Services you might want to consider:

Payday Loans

Payday loans are short-term loans that should be settled on your next payday. While they might seem convenient and quick to get, they usually have high-interest rates that may be unaffordable. If you’re considering using payday loans to get fast cash, be careful and think it through.

Personal Loans

Taking out a personal loan is a popular alternative to cash advances. Personal loans typically come with lower interest rates compared to payday loans. However, the approval process can take longer, and eligibility is typically contingent on a good credit score.

Unsecured Personal Loans

What course of action can you take if you need quick cash but lack collateral? Taking an unsecured personal loan can be a saviour in such circumstances.

Unsecured personal loans carry higher interest rates, and your eligibility for a substantial loan amount may be limited. It’s imperative to carefully consider the associated borrowing costs and evaluate your credit score to make informed choices.

Secured Personal Loans

Secured personal loans require collateral, as the name suggests. Lenders usually accept properties and cars as collateral, although it may vary.

Secured personal loans come with lower interest rates and allow for higher loan amounts compared to unsecured loans. However, if you fail to repay your loan, the lender has the right to take the collateral.

Credit cash advance interest can be costly, so the above-discussed options can be helpful. To avoid accruing penalties or losing your collateral, pay the loan promptly and steer clear of any potential issues.

What is a Credit Card Cash Advance?

How does cash advance work on credit cards? Credit card advances allow credit card holders to borrow against their credit limit, and the cash can be withdrawn from an ATM or bank and used as needed. However, they should be approached with caution due to high-interest rates and additional fees.

Typically, interest rates on credit card advances are higher than on traditional loans, and borrowers are charged an advance fee and ATM fee. Therefore, it’s a good practice to utilize a credit card advance only in emergency situations and to review the finer details carefully before proceeding.

Failure to pay this type of loan on time can attract significant negative consequences, such as additional fees, interest charges, and a negative impact on your credit score. To maintain financial stability, borrowers should plan on paying off the credit card cash advance promptly.

Before proceeding, cardholders should thoroughly understand what is considered a cash advance on a credit card and what to expect. A financial advisor can be an invaluable asset in this case. They can explain the potential costs and risks involved, suggest alternatives, and help them make informed financial decisions. Also, financial advisors can offer valuable advice to help you manage money wisely and avoid unnecessary debt.

How Can You Get Cash From Your Credit Card in Canada?

Can I take out cash from my credit card? Yes, you can. If you are seeking a solution to obtain immediate funds through your credit card in Canada, rest assured that we are here to assist you. Nonetheless, it is crucial to familiarize yourself with the pertinent terms, costs, and fees associated with each option before moving forward. So, how can I use my credit card to get cash? Here are the common methods for accessing cash from your credit card:

ATM Cash Advance

Are you aware that your credit card can be utilized to withdraw cash from an automated teller machine (ATM)? The process is fairly straightforward. Simply insert your card into the ATM, enter your personal identification number (PIN), and choose the cash advance option. However, exercise caution as cash advances typically entail substantial fees and interest rates. Therefore, it is advisable to proceed with care. To prevent any unforeseen circumstances, it’s essential to thoroughly review the terms and conditions of your credit card before using it for cash withdrawals.

Over-the-Counter Cash Advance

If you need funds and have a credit card, it is possible to seek an over-the-counter (OTC) cash advance from the respective issuing bank or financial institution. It is advisable to carry both your credit card and identification for expedited assistance. Upon arrival, a teller or customer service assistant will handle the necessary procedures. Similar to ATM cash advances, OTC cash advances are subject to fees and interest rates.

Balance Transfer to a Bank Account

Some credit cards come with an option to transfer cash from the credit card to a bank account, commonly referred to as a “balance transfer.” Following the completion of the transfer process, the cardholder can access the funds by withdrawing from an ATM or utilizing them in any other way.

Before initiating a balance transfer to a bank account, it’s prudent to inquire with your credit card provider regarding the availability of this feature and any associated fees. Also, bear in mind that fees may be applicable, and the interest rate on your credit card could potentially be impacted by the balance transfer.

Cash Convenience Checks

Cash convenience checks, as implied by their name, offer a convenient alternative as they function similarly to ordinary checks. This allows individuals to issue checks to themselves or others for specific amounts, which can subsequently be cashed. However, it is essential to pay close attention to the finer details.

Cardholders should thoroughly examine and comprehend the accompanying terms and conditions. There could be applicable fees or interest rates that necessitate careful consideration before utilizing these checks.

Retail Purchases with Cash Back

Many credit cards provide the added benefit of cash-back rewards for purchases made by cardholders. As a result, cardholders can request cash back at the point of sale when transacting with eligible retailers.

The process isn’t complicated— just request the cashier to include the amount you want to spend in your total purchase. That’s all. You will receive this sum in cash along with your purchase. Although this approach doesn’t get you cash directly from your credit card, it’s a convenient means to access funds promptly whenever the need arises.

How can you get cash from your credit card in Canada, Toronto? Now you’re familiar with this credit card feature and how it works. As a best practice, card cardholders should exercise discretion to choose an affordable option.

Advantages and Disadvantages of Credit Card Cash Advance

Credit Card Cash Advance Advantages

Credit card cash advances have both benefits and drawbacks. That said, you should carefully weigh your options for the best outcome. So, what is the advantage of a cash advance on a credit card?

Credit Card Cash Advance Advantages

Immediate Access to Funds

A credit card cash advance provides instant access to cash, eliminating the need for loan approvals or bank transfers.

Convenience

With a cash advance, you can obtain funds directly from your credit card, avoiding the hassle of visiting a bank or ATM.

Practical Support in Emergency Situations

Cash advances can be a lifeline during emergencies, providing quick financial assistance for unforeseen expenses like medical bills or car repairs.

No Collateral Required

Unlike certain borrowing methods, credit card cash advances usually don’t require collateral, making them accessible for individuals without valuable assets.

Flexibility in Fund Usage

Cash advances offer the freedom to allocate funds as needed, whether it’s paying bills, covering immediate expenses, or addressing unexpected costs.

A Good Credit Score isn’t Required

Cash advances often don’t involve a credit check, making them accessible for individuals with less-than-perfect credit scores.

Reward Points and Benefits

Some credit card companies offer rewards or loyalty points for cash advances, allowing you to earn benefits for future purchases or travel.

Consolidating High-interest Debt

Cash advances can help consolidate existing debts with high-interest rates into a single payment, potentially reducing overall interest and simplifying financial management.

Unrestricted Usage

Cash advances don’t come with usage restrictions, unlike certain loans, enabling you to address a wide range of financial needs or obligations.

Avoiding Bounced Checks and Late Fees

Cash advances can prevent bounced checks or late fees by providing funds to cover crucial payments when you’re short on cash.

So, is it wise to get a cash advance with a credit card? Credit card cash advances should be utilized as a last resort, particularly if it’s the only way to access cash in emergency situations. While credit card cash advances offer the above-mentioned advantages, it’s important to use them sparingly and explore alternative borrowing options whenever possible.

Credit Card Cash Advance Disadvantages

Credit card cash advances present numerous disadvantages that warrant careful consideration. Here are the disadvantages of cash advances.

High Fees

One major drawback of credit card cash advances is the imposition of high fees. Lenders typically charge substantial fees, often in the form of a percentage-based cash advance fee. These fees can quickly escalate the overall cost of the transaction, making cash advances an expensive borrowing option.

High-Interest Rates

Credit card cash advances have high-interest rates. These rates are typically higher than the interest rates for regular credit card purchases. As a result, borrowers end up incurring more interest charges.

The increased interest costs make cash advances an unfavourable option for those in need of financial assistance. Borrowers should carefully consider these high-interest rates and explore alternative borrowing options with lower rates to avoid accumulating excessive debt.

Immediate Interest Accrual

Unlike regular credit card purchases that may have a grace period, interest charges on cash advances start right after the transaction. This means that borrowers have to pay interest from the moment they receive the cash advance, regardless of when they plan to repay it. As a result, borrowers can end up paying more in interest, making cash advances an expensive borrowing option.

Absence of a Grace Period

For regular credit card purchases, you may have a period without interest. On the other hand, cash advances begin accruing interest right away. So even if you pay back the cash advance promptly, you still have to pay the interest that has already built up. Lack of a grace period means you’ll end up with higher interest charges, making cash advances a more expensive way to borrow money.

Limited Repayment Options

Credit card cash advances have limited repayment options, which is a major problem for many borrowers. When you make payments, credit card companies usually prioritize balances with lower interest rates, such as balance transfers or regular purchases.

As a result, if you have both a cash advance and these other balances, your payments will primarily go toward those balances first. Simply put, the high-interest cash advance balance will continue to accumulate interest, making it harder to repay and increasing the overall interest costs for the cash advance amount.

Negative Impact on Credit Score

Credit card cash advances can harm your credit score. They increase your credit utilization ratio, which is the amount of credit you’re using compared to your available credit. A high ratio can lower your credit score.

Moreover, frequently relying on cash advances suggests that you heavily depend on borrowed money, and this can be seen negatively by lenders and credit reporting agencies. Borrowers should be aware of these potential consequences and explore other options before resorting to a credit card cash advance.

Reduced Available Credit Limit

Credit card cash advances can reduce your available credit limit. The amount you borrow is deducted from your total available credit. Consequently, you’re left with less money to spend on other purchases or emergencies until you repay the cash advance and restore your credit limit.

Also, credit card cash advances can limit your financial flexibility. As a result, it will be challenging to handle unexpected expenses or make necessary transactions until the debt is settled.

Potential for Overborrowing

Credit card cash advances can increase borrowing appetite. The convenience of accessing immediate funds can make borrowing seem easy and tempting. This can lead to a habit of relying on credit rather than managing finances responsibly and saving money.

Credit card holders may start borrowing more than they can afford to repay. This habit may result in mounting debt and potential financial challenges in the future.

Cash Advance Traps

Credit card cash advances can trap unsuspecting borrowers. Many credit card companies lure customers with attractive offers but conveniently neglect to mention the exorbitant fees and interest rates that come with cash advances.

This lack of transparency eventually takes credit card holders into a cycle of debt that isn’t easy to break. As a best practice, you should read and comprehend the intricate terms and conditions before contemplating a credit card cash advance to avoid these deceptive traps.

Diminished Rewards and Benefits

Frequently using credit card cash advances can result in reduced rewards and benefits. Unlike regular credit card purchases, cash advances usually do not earn rewards like cash back or travel miles.

Moreover, some benefits provided by credit cards, such as purchase protection or extended warranties, may not apply to cash advance transactions. By opting for a cash advance, you may miss out on the opportunity to earn rewards and access additional benefits that are typically associated with regular credit card usage.

Heightened Risk of Identity Theft

Credit card cash advances raise the risk of identity theft. Carrying a substantial amount of cash obtained from a cash advance makes you more susceptible to theft or loss. Unlike a lost or stolen credit card, recovering cash is extremely challenging.

Borrowers can incur significant financial losses and become victims of personal identity theft. That said, you must be cautious by taking necessary precautions when carrying large sums of cash obtained through credit card cash advances.

Promotes Impulsive Spending

The immediate availability of cash can tempt individuals into impulsive purchases of non-essential items. This can exacerbate their financial situation, making it more challenging to repay the borrowed amount.

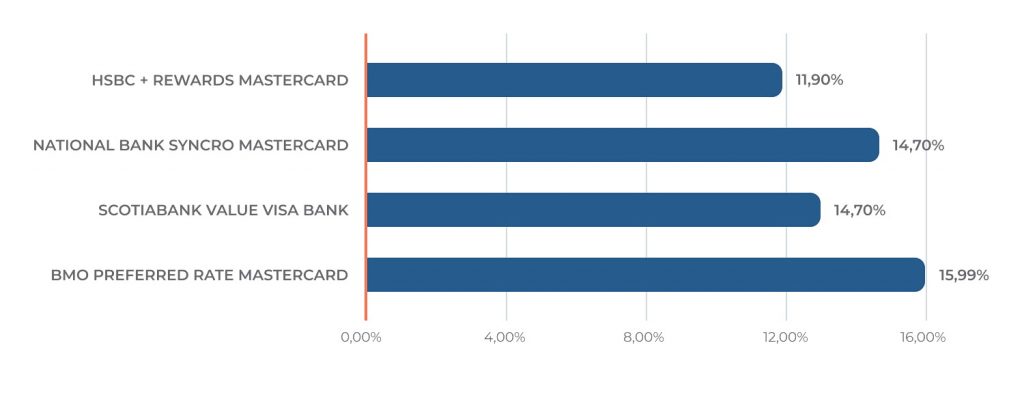

Credit Card Cash Advance Interest Rate

Credit card cash advances come with higher interest rates compared to regular credit card purchases. These rates usually range between 20% to 23%. The rates can vary by credit card issuer and specific terms. Unlike regular purchases, interest accrues immediately after you withdraw the cash without any grace period. Borrowers must be mindful of these high costs of cash advances.

Credit Card Cash Advance Interest Rate

Credit card cash advances can be a real lifesaver when you’re in a pinch. But hold on just a second – before you go rushing off to get one. It’s absolutely important to keep in mind the interest rate.

Unfortunately, cash advances typically come with a higher interest rate than regular purchases, which means you’ll end up paying more in the long run. In fact, these interest rates are way higher than what you’d pay for a regular purchase. Why? Well, because they’re seen as riskier and are usually a last resort for people who really need cash fast.

Cash Advance Interest Rates Compared

Alternatives to Cash Advance From Credit Card

Unsecured Personal Loan or Line of Credit – Traditional Lender

Traditional lenders, such as banks, credit unions, or online lenders, offer unsecured personal loans or lines of credit. These loans don’t require collateral and can be used for different purposes, like consolidating debt or covering significant expenses. However, an eligibility criterion must be met, including demonstrating good creditworthiness and providing proof of income, to increase your chances of approval for these loans.

| Cash Advance | Unsecured Personal Loan or Line of Credit – Traditional Lender | |

| PROS |

|

|

| CONS |

|

|

| Cash Advance |

| PROS |

|

| CONS |

|

| Unsecured Personal Loan or Line of Credit – Traditional Lender |

| PROS |

|

| CONS |

|

Secured Loan or Line of Credit – Traditional Lender

A line of credit from a traditional lender is a loan facility that requires collateral, like a house, car, or savings account. By having collateral, lenders have more security in case you can’t repay the loan.

These loans have lower interest rates and allow you to borrow larger amounts of money. You can use them for things like home improvements or buying a car. However, if you default on the repayments, you could lose the collateral. Applying for secured loans or line of credit loans typically involves more paperwork. So, the process may take longer because the lender needs to evaluate the collateral you’re providing.

| Cash Advance | Secured Loan or Line of Credit – Traditional Lender | |

| PROS |

|

|

| CONS |

|

|

| Cash Advance |

| PROS |

|

| CONS |

|

| Secured Loan or Line of Credit – Traditional Lender |

| PROS |

|

| CONS |

|

Personal Loan – Non-Traditional Lender

Nontraditional lenders offer personal loans as an alternative option for people who can’t get approved for traditional bank loans. These lenders operate online or through peer-to-peer networks, making the application process quicker.

Nontraditional lenders often charge higher interest rates because they lend to people with limited credit history or lower credit scores. They may also add extra fees like origination fees, which increase the overall cost of borrowing. For the best outcome, borrowers should carefully review the loan terms to make informed decisions. Transparency is key when reviewing these loans.

| Cash Advance | Personal Loan – Non-Traditional Lender | |

| PROS |

|

|

| CONS |

|

|

| Cash Advance |

| PROS |

|

| CONS |

|

| Personal Loan – Non-Traditional Lender |

| PROS |

|

| CONS |

|

Payday Loan

A payday loan is a short-term, high-interest loan generally due when the borrower is paid next. The loan amount is usually based on the borrower’s income and is meant to provide quick access to cash in emergency situations. However, payday loans often come with extremely high fees and interest rates, making them a costly form of borrowing. They should only be considered as a last resort, and credit card holders should be cautious when taking these types of loans.

| Cash Advance | Payday Loan | |

| PROS |

|

|

| CONS |

|

|

| Cash Advance |

| PROS |

|

| CONS |

|

| Payday Loan |

| PROS |

|

| CONS |

|